Oklahoma Car Insurance Requirements: What Most Drivers Get Wrong

Many Oklahoma drivers assume having “basic insurance” means they’re fully meeting state requirements. But car insurance laws vary significantly from state to state, and misunderstandings about Oklahoma’s minimum requirements are more common than many people realize.

Some drivers believe “full coverage” is legally required. Others assume insurance only matters if a vehicle is financed. In reality, Oklahoma has relatively straightforward car insurance laws — but understanding them is important if you want to stay compliant and avoid penalties.

Because Oklahoma uses a fault-based insurance system, drivers are legally required to carry minimum liability insurance to help cover damages they may cause in an accident. Failing to maintain coverage can lead to fines, suspended registration, and other legal consequences.

This guide explains Oklahoma car insurance requirements, how they compare to nearby states, and the most common misunderstandings drivers have about Oklahoma insurance laws.

Quick Answer: What Insurance Is Required in Oklahoma?

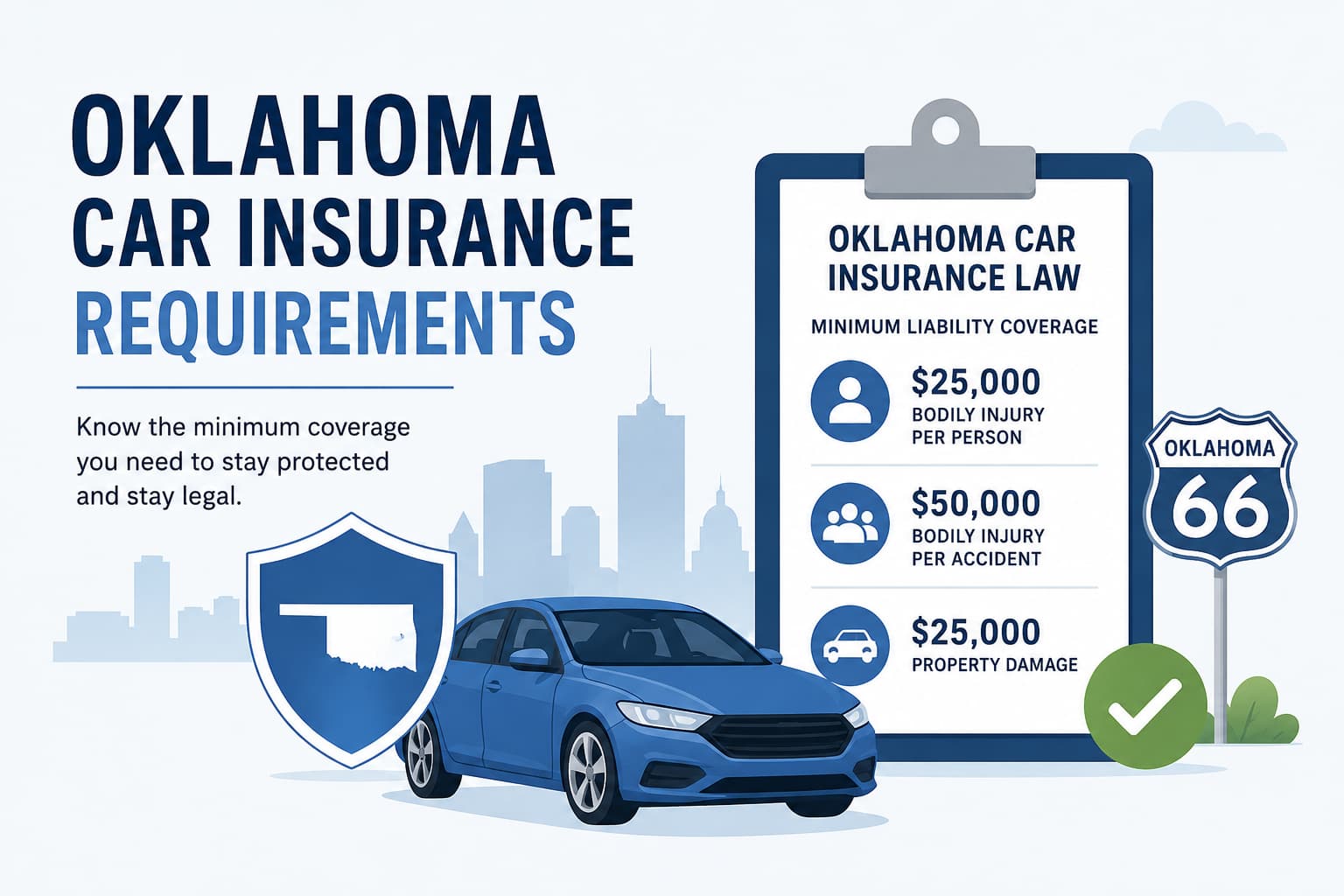

Oklahoma requires drivers to carry minimum liability insurance coverage of:

- $25,000 for bodily injury liability per person

- $50,000 for bodily injury liability per accident

- $25,000 for property damage liability

This is commonly referred to as 25/50/25 coverage.

These are the minimum liability insurance limits required to legally operate a vehicle in Oklahoma.

GET A QUOTE

Enter Zip Code Below

Key Takeaways About Oklahoma Car Insurance Requirements

- Oklahoma is a fault-based insurance state

- Liability insurance is legally required for most drivers

- Oklahoma minimum coverage limits are 25/50/25

- “Full coverage” is not required by Oklahoma law

- Insurance requirements differ from state to state

- Driving without insurance may result in fines, suspension, or SR-22 requirements

Why Car Insurance Requirements Differ by State

Car insurance laws are regulated at the state level, which is why requirements vary across the country.

Each state sets its own rules based on factors such as:

- accident rates

- population density

- medical costs

- uninsured driver statistics

- legal systems and claim environments

For example, Florida uses a no-fault insurance system, while Oklahoma uses a traditional fault-based system.

That distinction matters because it changes how accident claims are handled and what coverage drivers must legally carry.

Oklahoma Is a Fault-Based Insurance State

Oklahoma follows a fault-based (or “tort”) insurance system.

This means the driver responsible for causing an accident may also be financially responsible for resulting damages.

Because of this system, Oklahoma requires drivers to carry liability insurance that can help cover:

- injuries to other people

- damage to another person’s vehicle or property

Many drivers moving from other states are surprised to learn that insurance laws can change significantly depending on where they live.

For example, neighboring Texas requires higher bodily injury liability limits than Oklahoma, while Kansas requires additional personal injury protection (PIP) coverage.

Oklahoma Minimum Liability Insurance Requirements Explained

Many drivers see “25/50/25” online or on insurance documents without fully understanding what those numbers mean.

Here’s a simple breakdown of Oklahoma’s minimum car insurance requirements.

$25,000 Bodily Injury Liability Per Person

This coverage helps pay for injuries to another person if you cause an accident.

Example:

If one person is injured in an at-fault accident, your liability policy may help cover eligible expenses up to $25,000.

$50,000 Bodily Injury Liability Per Accident

This is the total amount available for all bodily injury claims combined in a single accident.

Example:

If multiple people are injured, the maximum payout for all injuries together would generally be capped at $50,000.

$25,000 Property Damage Liability

This coverage helps pay for damage you cause to another person’s:

- vehicle

- fence

- building

- mailbox

- sign

- other property

Property damage liability is one of the most commonly used portions of a liability policy after an accident.

What Oklahoma Liability Insurance Covers

Oklahoma minimum liability insurance is designed to help cover damages you may cause to others.

It generally helps pay for:

- bodily injuries to other drivers or passengers

- property damage to another vehicle

- certain accident-related legal expenses

However, Oklahoma’s required liability coverage generally does not cover:

- damage to your own vehicle

- theft

- hail damage

- flooding

- vandalism

This is one of the biggest misunderstandings Oklahoma drivers have about minimum insurance requirements.

Common Misunderstandings About Oklahoma Insurance Laws

Misunderstanding #1: “Full Coverage” Is Required

One of the most common myths is that Oklahoma law requires full coverage insurance.

It does not.

Oklahoma law generally requires liability insurance only.

However, banks and lenders often require additional coverage for financed or leased vehicles. That requirement comes from the lender — not the state.

Misunderstanding #2: Older Cars Don’t Need Insurance

Some drivers assume insurance becomes optional once a vehicle is fully paid off.

That is incorrect.

Even older vehicles typically must carry Oklahoma’s minimum liability coverage if driven on public roads.

Misunderstanding #3: Oklahoma and Texas Have the Same Insurance Requirements

Insurance laws vary widely by state.

Here’s how Oklahoma compares to nearby states:

| State |

Minimum Liability Requirements |

| Oklahoma |

25/50/25 |

| Texas |

30/60/25 |

| Arkansas |

25/50/25 |

| Kansas |

25/50/25 + PIP coverage |

Drivers relocating to Oklahoma should make sure their insurance policy meets Oklahoma requirements.

Misunderstanding #4: Proof of Insurance Alone Means You’re Compliant

Having an old insurance card does not necessarily mean coverage is active.

Oklahoma drivers are required to maintain continuous insurance coverage. Policy cancellations or lapses can still lead to penalties, even if you previously carried insurance.

Oklahoma Uses Electronic Insurance Verification

Oklahoma uses an electronic insurance verification system to monitor compliance with state insurance laws.

Law enforcement officers may electronically verify active coverage during:

- traffic stops

- registration checks

- accident investigations

This system is designed to identify uninsured vehicles and improve compliance with Oklahoma financial responsibility laws.

For drivers, this means maintaining active insurance coverage is important even if physical proof of insurance is available.

Penalties for Driving Without Insurance in Oklahoma

Driving without required insurance in Oklahoma can lead to several penalties.

Potential consequences may include:

- fines

- suspended vehicle registration

- driver’s license suspension

- reinstatement fees

- possible SR-22 filing requirements

According to the Insurance Information Institute (III), uninsured driving remains a significant issue nationwide, which is one reason states continue enforcing mandatory liability insurance laws.

The Insurance Research Council has also reported that uninsured motorist rates in several Southern states remain above the national average, contributing to stricter enforcement efforts in many areas.

Why Oklahoma Requires Liability Insurance

Liability insurance requirements are intended to establish financial responsibility after accidents.

Without minimum insurance laws, drivers involved in accidents could face significant difficulty paying for injuries or property damage caused to others.

In Oklahoma’s fault-based system, liability insurance helps create a financial framework for handling accident-related claims and damages.

While Oklahoma’s requirements are relatively straightforward compared to some states, understanding how they work can help drivers avoid compliance issues and legal penalties.

Frequently Asked Questions About Oklahoma Car Insurance Requirements

Is car insurance required in Oklahoma?

Yes. Oklahoma law requires drivers to carry minimum liability insurance coverage to legally operate most vehicles on public roads.

What is the minimum car insurance requirement in Oklahoma?

Oklahoma requires:

- $25,000 bodily injury liability per person

- $50,000 bodily injury liability per accident

- $25,000 property damage liability

This is commonly referred to as 25/50/25 coverage.

Is full coverage required in Oklahoma?

No. Oklahoma law generally requires liability insurance only. Additional coverage requirements may apply if a vehicle is financed or leased.

What happens if you drive without insurance in Oklahoma?

Drivers may face fines, suspended driving privileges, registration suspension, reinstatement fees, and possible SR-22 filing requirements.

Does Oklahoma accept digital proof of insurance?

Yes. Oklahoma generally allows drivers to show digital proof of insurance during traffic stops or registration checks.

Final Thoughts

Oklahoma’s car insurance requirements are relatively straightforward, but many drivers still misunderstand what the law actually requires.

Common misconceptions include:

- believing full coverage is mandatory

- assuming older vehicles don’t need insurance

- thinking insurance laws are the same in every state

- assuming proof of insurance always means coverage is active

Understanding Oklahoma’s minimum liability insurance requirements can help drivers stay compliant, avoid penalties, and avoid costly lapses in coverage.

At Cheapest Auto Insurance, we help Oklahoma drivers quickly compare affordable policies that meet the state’s minimum insurance requirements — without overcomplicating the process. Whether you need basic liability coverage to stay legal on the road or you’re looking for a low-cost policy that fits your budget, comparing quotes can help you find coverage that works for your situation.

If you’re unsure whether your current policy meets Oklahoma’s requirements, it may be a good time to review your coverage and compare available rates.